Accrue Investment Management Meet Neil Woodford

Martin Badder went to meet Neil for a question and answer session about The CF Woodford Equity Income Fund. Here’s the latest fund round-up:

Last year’s challenges remained largely intact during the first month of 2015 with markets continuing to focus on falling energy prices and geopolitical tensions. The further decline in the price of crude oil set the tone for a volatile month, weighing on energy-related stocks and causing concern about the health of the global economy.

In the second half of the month, attention switched towards Europe following the Greek election of the far-left radical party, Syriza, which is committed to ending years of painful austerity. This potentially heralds a period of further political and economic uncertainty in Europe, where several other nations have seen populist parties gaining traction at the expense of more mainstream politics and substantially increases the risk of a Greek sovereign bond default. Elsewhere in Europe, Switzerland’s central bank unexpectedly ditched its peg to the euro, leading to an immediate and substantial surge in the value of the Swiss franc.

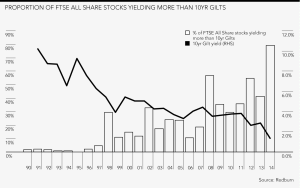

The eurozone is now in outright deflation and whilst many economists expect inflation rates to remain negative only temporarily, we are not so convinced. The threat of an entrenched deflationary mindset engulfing the eurozone appears significant enough to have finally convinced the Germans to reluctantly support a European Central Bank (ECB) programme of Quantitative Easing (QE). In turn, sovereign bond yields continued to decline, with UK 10 year Gilt yields falling to new lows towards the end of the month. 10 year Gilts are now yielding well below 2.0%, the proportion of UK stocks yielding more than Gilts has never been higher.

Athough this is a clear indication of the income attractions of the equity asset class, it is worth bearing in mind the reasons why bond yields are so low before becoming too enthusiastic. The bond market is evidently worried about the health of the global economy. Ultra-low sovereign bond yields reflect growing concern about the ‘Japanification’ of the western world, Europe in particular. In turn this would imply an extremely challenging trading environment for many businesses, and suggests investors need to be as selective as ever and focused on dividend sustainability, rather than headline yield alone.

One of the most dependable sources of dividend income for the equity investor is the tobacco sector, which features prominently in the portfolio. Over the last 25 years, the tobacco sector has an unsurpassed track record of delivering superior long-term total returns1 based on attractive starting yields and consistent, sustainable dividend growth. In January, our tobacco holdings performed very robustly, with significant contributions from Imperial Tobacco, British American Tobacco and Reynolds American, the latter assisted further by the strength of the dollar versus sterling.

Pharmaceuticals also performed well, with positive contributions from GlaxoSmithKline, AstraZeneca, Sanofi and a number of our smaller biotech positions. US biotech firm Alkermes was particularly strong, after two of its drugs – designed to treat clinical depression and schizophrenia – produced positive results in clinical trials. We view these positive trial results as potentially very significant developments and further evidence of the strength of Alkermes’ pipeline.

Allied Minds and IP Group also performed well – both specialise in the commercialisation of intellectual property and help to nurture early-stage businesses through to commercial success. The market is steadily warming to the long-term growth potential that exists within these businesses.

The largest detractor from performance was Drax, which continued to suffer from the government’s announcement in December that it is consulting on changes to its stance towards the support of biomass conversion projects. Although this is frustrating and disappointing, we remain convinced of the long-term investment case, given the quality of its management team, low valuation and the clear economic advantage of biomass compared to other sources of renewable energy. Drax’s shares recovered somewhat towards the end of the month after the European Union approved UK government support for a competitor’s biomass power station. We progressively added to our holding throughout the month.

Another significant detractor was Game Digital. The video games retailer issued a profit warning during the month, pointing to fierce competition during the Christmas period. This was disappointing, but one poor trading update does not undermine what we see as a strong long-term investment case. The shares fell immediately and sharply after the warning and we took advantage of this by materially adding to our holding at what we believe to be very attractive valuation levels.

We initiated a new position in P2P Global Investments during the month by participating in its C share issue. The company invests in online peer-to-peer lending credit assets and its proprietary technology system allows it to seek out the highest quality loans from a wide variety of platforms. The company looks well-placed to deliver a consistently attractive income stream to its investors.

We also added a new unquoted position to the portfolio during January. Novabiotics is a biotechnology company with two lead products in clinical trials: Novexatin is a topical (brush on) nail fungus treatment in Phase II trials partnered with Taro Pharmaceuticals; Lynovex is a treatment for Cystic Fibrosis also in Phase II trials. We believe Novabiotics is another great example of an exciting and innovative early-stage British business, based on excellent science and strong intellectual property, which offers the prospect of significant long-term growth should it fulfil its potential.

Elsewhere, we added active investment fund Crystal Amber to the portfolio during the month. This is a company that we have known well for a long time and we are very supportive of its investment approach which aims to deliver long-term value through active engagement with the companies in which it has invested. We hold its management team in very high regard.

We also added to a number of other existing positions including Spire Healthcare in an attractively discounted share placing, Utilitywise into share price weakness, Babcock International where a site visit helped to further build our conviction in the long-term investment case, and Centrica & SSE as further political interference caused renewed share price weakness in the energy utility sector.

We sold out of our position in Gagfah, the German real estate business during the month. Having received a bid from larger competitor Deutsche Annington in December, we took the opportunity to sell our holding. Another company subject to recent bid speculation is Smith & Nephew, which we also sold with its shares trading near all-time highs. Clearly, if a bid were to materialise, it could lift the share price higher still but we believe other opportunities now offer greater long-term income potential.

Source: Bloomberg

Martin Badder went to meet Neil for a question and answer session about The CF Woodford Equity Income Fund. Here’s the latest fund round-up:

Last year’s challenges remained largely intact during the first month of 2015 with markets continuing to focus on falling energy prices and geopolitical tensions. The further decline in the price of crude oil set the tone for a volatile month, weighing on energy-related stocks and causing concern about the health of the global economy.

In the second half of the month, attention switched towards Europe following the Greek election of the far-left radical party, Syriza, which is committed to ending years of painful austerity. This potentially heralds a period of further political and economic uncertainty in Europe, where several other nations have seen populist parties gaining traction at the expense of more mainstream politics and substantially increases the risk of a Greek sovereign bond default. Elsewhere in Europe, Switzerland’s central bank unexpectedly ditched its peg to the euro, leading to an immediate and substantial surge in the value of the Swiss franc.

The eurozone is now in outright deflation and whilst many economists expect inflation rates to remain negative only temporarily, we are not so convinced. The threat of an entrenched deflationary mindset engulfing the eurozone appears significant enough to have finally convinced the Germans to reluctantly support a European Central Bank (ECB) programme of Quantitative Easing (QE). In turn, sovereign bond yields continued to decline, with UK 10 year Gilt yields falling to new lows towards the end of the month. 10 year Gilts are now yielding well below 2.0%, the proportion of UK stocks yielding more than Gilts has never been higher.

Athough this is a clear indication of the income attractions of the equity asset class, it is worth bearing in mind the reasons why bond yields are so low before becoming too enthusiastic. The bond market is evidently worried about the health of the global economy. Ultra-low sovereign bond yields reflect growing concern about the ‘Japanification’ of the western world, Europe in particular. In turn this would imply an extremely challenging trading environment for many businesses, and suggests investors need to be as selective as ever and focused on dividend sustainability, rather than headline yield alone.

One of the most dependable sources of dividend income for the equity investor is the tobacco sector, which features prominently in the portfolio. Over the last 25 years, the tobacco sector has an unsurpassed track record of delivering superior long-term total returns1 based on attractive starting yields and consistent, sustainable dividend growth. In January, our tobacco holdings performed very robustly, with significant contributions from Imperial Tobacco, British American Tobacco and Reynolds American, the latter assisted further by the strength of the dollar versus sterling.

Pharmaceuticals also performed well, with positive contributions from GlaxoSmithKline, AstraZeneca, Sanofi and a number of our smaller biotech positions. US biotech firm Alkermes was particularly strong, after two of its drugs – designed to treat clinical depression and schizophrenia – produced positive results in clinical trials. We view these positive trial results as potentially very significant developments and further evidence of the strength of Alkermes’ pipeline.

Allied Minds and IP Group also performed well – both specialise in the commercialisation of intellectual property and help to nurture early-stage businesses through to commercial success. The market is steadily warming to the long-term growth potential that exists within these businesses.

The largest detractor from performance was Drax, which continued to suffer from the government’s announcement in December that it is consulting on changes to its stance towards the support of biomass conversion projects. Although this is frustrating and disappointing, we remain convinced of the long-term investment case, given the quality of its management team, low valuation and the clear economic advantage of biomass compared to other sources of renewable energy. Drax’s shares recovered somewhat towards the end of the month after the European Union approved UK government support for a competitor’s biomass power station. We progressively added to our holding throughout the month.

Another significant detractor was Game Digital. The video games retailer issued a profit warning during the month, pointing to fierce competition during the Christmas period. This was disappointing, but one poor trading update does not undermine what we see as a strong long-term investment case. The shares fell immediately and sharply after the warning and we took advantage of this by materially adding to our holding at what we believe to be very attractive valuation levels.

We initiated a new position in P2P Global Investments during the month by participating in its C share issue. The company invests in online peer-to-peer lending credit assets and its proprietary technology system allows it to seek out the highest quality loans from a wide variety of platforms. The company looks well-placed to deliver a consistently attractive income stream to its investors.

We also added a new unquoted position to the portfolio during January. Novabiotics is a biotechnology company with two lead products in clinical trials: Novexatin is a topical (brush on) nail fungus treatment in Phase II trials partnered with Taro Pharmaceuticals; Lynovex is a treatment for Cystic Fibrosis also in Phase II trials. We believe Novabiotics is another great example of an exciting and innovative early-stage British business, based on excellent science and strong intellectual property, which offers the prospect of significant long-term growth should it fulfil its potential.

Elsewhere, we added active investment fund Crystal Amber to the portfolio during the month. This is a company that we have known well for a long time and we are very supportive of its investment approach which aims to deliver long-term value through active engagement with the companies in which it has invested. We hold its management team in very high regard.

We also added to a number of other existing positions including Spire Healthcare in an attractively discounted share placing, Utilitywise into share price weakness, Babcock International where a site visit helped to further build our conviction in the long-term investment case, and Centrica & SSE as further political interference caused renewed share price weakness in the energy utility sector.

We sold out of our position in Gagfah, the German real estate business during the month. Having received a bid from larger competitor Deutsche Annington in December, we took the opportunity to sell our holding. Another company subject to recent bid speculation is Smith & Nephew, which we also sold with its shares trading near all-time highs. Clearly, if a bid were to materialise, it could lift the share price higher still but we believe other opportunities now offer greater long-term income potential.

Source: Bloomberg